Let me tell you a story about a friend who did not create a rainy day fund. Once, I had a friend named Jasmine; she had recently landed a high-paying job in a tech company which she deserved as all her childhood, she did not have the things she wanted as she was raised by a single mother who found it difficult to make ends meet. Jasmine was never taught the art of saving, and as soon as she got her first salary, she went on a shopping spree and bought everything she wanted, new clothes, watches, and perfumes, and spent money on things she did not need.

During the covid-19 pandemic, she lost her job as the tech company shut down. She could not make ends meet because she did not create a rainy day fund and suffered a lot to afford basic necessities. If only she had created a rainy day fund.

In this article, I will show you the basic steps to create a rainy day fund so, god forbid, in times of trouble, you have a backup plan to pull yourself out.

How to create a rainy day fund

Rainy day funds are like secret treasures hidden away for those unexpected storms that life throws at us. Although it may seem like a rainy day will never come, being prepared is the key to financial peace of mind. So, let’s imagine you’re comfortably settled on your favorite couch, and I’ll take you on a journey through the steps to create your own rainy day fund.

Picture this: life is full of surprises, both good and bad. Unexpected expenses can sneak up on us when we least expect them, like a sudden downpour on a sunny day. But fear not! A rainy day fund acts as your trusty umbrella, shielding you from financial setbacks and keeping you dry when those bills pour in.

Now, step one on this adventure is to understand the purpose of a rainy day fund. It’s not just about saving for a specific goal or dream vacation (although those are important, too!). This fund is your safety net, a cushion to help you navigate unexpected expenses without using high-interest loans or credit cards.

Now, grab a cozy blanket, snuggle up on that couch, and let the rain fall outside while you bask in the warmth of your well-prepared rainy day fund. Your financial future will thank you for it

1. Calculating Your Monthly Expenses

Now, here we need to calculate how much of our income we spend on your monthly expenses. Let’s say your monthly income from your salary is $100; from this amount, you spend $50 on food, water, rent, and monthly groceries. You are now left with $50 from the amount you pay for your car’s monthly maintenance and leisure, like going to a restaurant or the cinema, costing you about $35. You are then left with $15. Now, you need to do something productive from this amount, like saving it for a rainy day. It would be best to calculate how much you spend and how much you are left with in summary, so sit down with a pen and a piece of paper.

2. The 50/30/20 Rule

This rule is a lifesaver and proves to be one for decades for those who want a secure future and never die hungry with no money in the bank. Here it is simply what you need to do is spend 50% of your money on requirements, 30% on wants, and 20% on savings is a general principle. Find out more about the 50/30/20 budget rule and decide if it applies to you.

Practical Example

Let me make your life easier and help you understand this concept more practically:

Following her college graduation, Sophie was hired for her first job. At last, she was overjoyed to have her own income, but she wasn’t sure how to handle it. She had always relied on her parents to cover her bills, so when she found herself on her own, the idea of creating a budget and starting to save made her feel anxious.

She learned about the 50-30-20 rule from a friend one day. Sophie decided to try it since she was curious. She took her $3,000 monthly salary and divided it into three categories:

Needs

50% for needs: Sophie estimated her monthly costs to be $1,500, which included her rent, utilities, groceries, transportation, and insurance. She felt relieved that her necessary costs quickly fell within the 50% group. Here is how you reduce your monthly bills to spend under 50% of your income.

Wants

30% for wants: Sophie knew she liked dining and watching movies with her friends. So she set aside $900 for luxuries. She understood she could still pamper herself and have fun without going bankrupt.

Savings

20% for savings or clearing out her debts: From her income. Sophie put aside $600 to pay her loans if she had taken any or to save just in case she lost her job. For unexpected events like these, she made use of this 20%. Here you can learn how to create a saving plan for a prosperous future. But remember, only savings are not enough. It will have an inflation effect. You need to invest it. Here are some guides on how to invest your money in mutual funds.

Sophie was intelligent and stuck to her plan of following the 50-30-20 rule. She was able to enjoy her social life, live within her means, and save money for her future objectives. She eventually even began investing some of her money, knowing that the 20% she was laying aside would help her create a stable financial future. Sophie could take charge of her finances and felt more secure about her financial future due to the 50-30-20 rule.

For your convenience, I have also attached a YouTube video on how to create a rainy-day fund

This 4-minute YouTube video by the channel N26 teaches you a very interactive and creative way to create a rainy day fund. Do give it a watch.

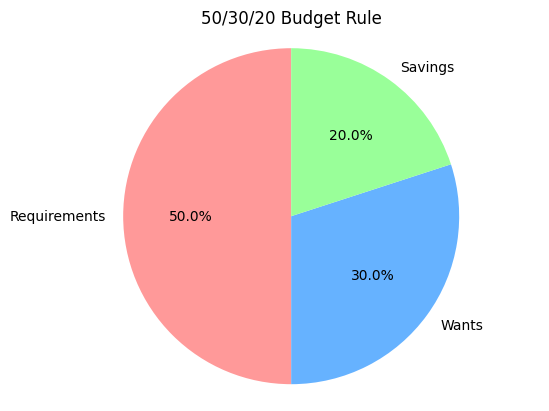

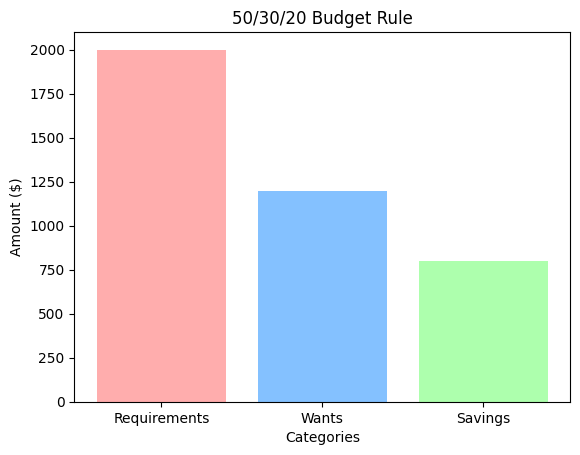

50/30/20 Rule Budgeting Example

In this example, let’s say your monthly income is $4,000. Following the 50/30/20 budget rule:

- 50% of your income, which is $2,000, would be allocated to requirements such as rent/mortgage, utilities, groceries, and other essential expenses.

- 30% of your income, which is $1,200, would be dedicated to wants, allowing you to indulge in non-essential items like dining out, entertainment, or hobbies.

- 20% of your income, which is $800, would be saved for the future, whether it’s for an emergency fund, retirement savings, or other financial goals.

Now that you understand the 50/30/20 budget rule and a pie chart example, you can assess whether it aligns with your financial situation and goals. It’s always a good idea to tailor your budgeting approach to your unique circumstances, ensuring a secure future and peace of mind

3. Forecasting your rainy day fund

A rainy day fund should not be lavish. It would help you survive through time wear, which does not have a steady income. So, thinking about leisure spending is out of the box. From the expenses, you had calculated for yourself. You would now need to forecast and make a budget for your rainy day fund, covering the food, water, gas, heating, electricity, and clothing you survive. This budget would mean you would need to save as much as possible.

It’s a friendly piece of advice to you, my friend, that start creating a fund instead of regretting it will lead you to a prosperous and distressful future.

Welcome to the Happy World!

Finally, setting up a rainy day fund is essential to financial planning that can offer protection and peace of mind when unforeseen needs happen. You may prevent using up your savings or incurring debt by adhering to the 50-30-20 rule and keeping money away, particularly for emergencies. And may create and maintain a rainy day fund that will help you weather any financial storm with a sound budget, consistent contributions, and wise investing strategies. You can create a rainy day fund by following these steps, reading the linked articles, and watching YouTube videos. It is the best safety plan on your side, as one should always have a plan B.

{kind=link}